Convex Optimization

10. Convex Optimization#

This chapter provides general introduction to convex optimization problems. Convex optimization focuses on a special class of mathematical optimization problems where:

The real valued function being optimized (maximized or minimized) is convex.

The feasible set of values for the function is a closed convex set.

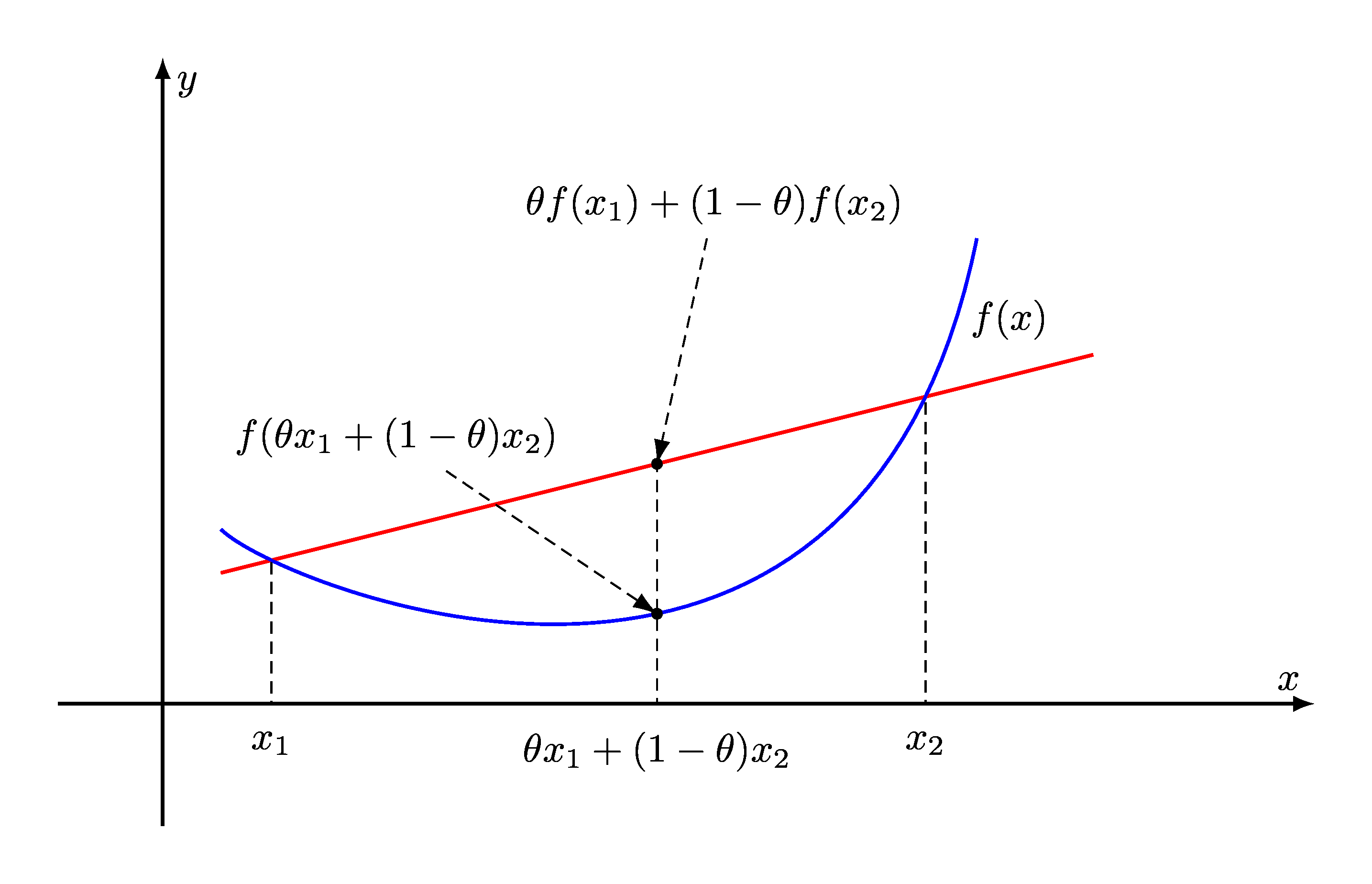

Fig. 10.1 For a convex function, the line segment between any two points on the graph of the function does not lie below the graph between the two points. Its epigraph is a convex set. A local minimum of a convex function is also a global minimum.#

Convex optimization problems are usually further classified into

Least squares

Linear programming

Quadratic minimization with linear constraints

Quadratic minimization with convex quadratic constraints

Conic optimization

Geometric programming

Second order cone programming

Semidefinite programming

There are specialized algorithms available for each of these classes.

Some of the applications of convex optimization include:

Portfolio optimization

Worst case risk analysis

Compressive sensing

Statistical regression

Model fitting

Combinatorial Optimization